{kind=link}

Table of Contents

Most people don’t have a saving problem. They have a starting problem.

You know you should be saving money. You’ve read the articles, you’ve nodded along to the advice, and then the month ends and somehow the account is back to zero. That’s not a lack of discipline — it’s a lack of systems. The good news: once the right habits are in place, saving money stops being a struggle and starts being automatic. This guide covers easy ways to save money that actually work in real life, whether you’re comfortable or just getting by.

Start With a Budget That’s Actually Honest

Before you can save money, you need to know where it’s going. Most people are shocked when they really look.

Pull up your credit card and bank statements from the last two or three months. Go line by line. Don’t estimate — look at the real numbers. You’ll almost always find a few places where you’re spending more than you thought: food delivery, subscriptions you forgot about, impulse buys that added up over time.

Build a Budget That Reflects Real Life

A budget only works if it reflects how you actually live, not how you wish you lived. Use the 50/30/20 rule as a starting point: 50% of your take-home pay on needs, 30% on wants, and 20% toward savings and debt. Adjust from there.

The goal isn’t perfection — it’s awareness. When you review your budget monthly, overspend becomes visible. Visible problems are fixable problems.

Quick steps to build your budget:

- List every source of income (after tax)

- List all fixed monthly bills (rent, utilities, insurance, subscriptions)

- Track variable spending (groceries, gas, dining out) over one full month

- Find the gap between what comes in and what goes out

- Assign that gap a job — savings, debt payoff, or both

Set Your Savings Goals Before You Spend Anything

Here’s a mindset shift that changes everything: treat saving money like a bill you pay yourself first.

Most people save whatever’s left at the end of the month. That’s backwards. Set your savings goals at the start of the month, transfer that amount out immediately, and then live on what remains. You’ll be surprised how quickly you stop missing it.

Be specific about what you’re saving for. “I want to save money” is vague. “I want $5,000 in an emergency fund by December” is a target. Savings goals with a number and a deadline are dramatically easier to stick to, because they give you a reason to say no to things that don’t serve them.

Automate Your Savings So You Never Miss a Transfer

Willpower is unreliable. Automation isn’t.

Set up automatic transfers from your checking account to your savings account right after every paycheck. Even a small amount — $25, $50, $100 — adds up faster than you’d expect. After a few months, you’ll barely notice the transfer happening, but your savings balance will keep climbing.

Many banks offer round-up features that sweep spare change into savings whenever you spend. If you buy a coffee for $3.40, the app rounds up to $4 and deposits the extra $0.60 into savings. Small amounts like that can add up to hundreds of dollars annually without any effort.

High-Yield Savings Accounts Are Worth the Switch

If your savings are sitting in a standard checking or savings account earning next to nothing, you’re leaving money behind. High-yield savings accounts offered through online banks can earn significantly more in interest — sometimes 10 to 20 times the national average rate.

The switch takes about 15 minutes. You keep the same habits, use the same automatic deposit, and your money just grows faster. That’s one of the simplest ways to grow your savings without changing your lifestyle at all.

Cut Expenses Where the Numbers Are Biggest

Skipping your morning coffee won’t save you. Skipping a $180/month subscription you never use will.

Before cutting small things, go after the big monthly expenses. These are the places where even a single change can lead to significant savings.

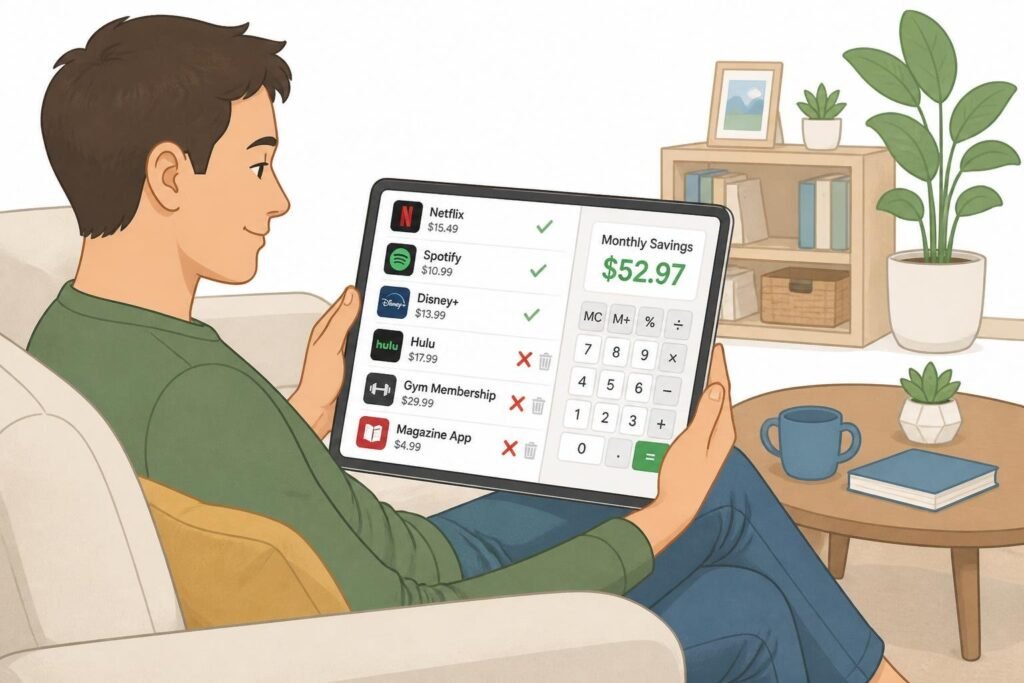

Review Your Subscriptions

Most households are subscribed to at least two or three services they’ve forgotten about. Streaming platforms, gym memberships, software trials, premium app tiers — it’s easy to rack up $100+ per month in subscription charges that quietly drain your account.

Go through your bank and credit card statements and flag every recurring charge. Cancel anything you haven’t used in the last 30 days. Pause what you’re not sure about. You can always resubscribe, but you can’t get back what you already paid.

Refinance to a Lower Interest Rate

If you’re carrying a mortgage, car loan, or student debt, it might be time to refinance. Interest rates shift over time, and a lower interest rate on a large loan can save you thousands in interest over time. Run the numbers before assuming it’s not worth it.

Refinancing your mortgage by even 0.5% on a $300,000 loan can save you hundreds of dollars per month and tens of thousands over the life of the loan. That’s not a rounding error.

Reduce Your Energy Costs at Home

Monthly bills for electricity and gas are easy to overlook because they feel fixed. They’re not. Small changes — switching to LED bulbs, using fans instead of air conditioning when possible, adjusting your thermostat by two degrees, unplugging devices on standby — can reduce your energy costs by $20 to $50 per month. That’s $240 to $600 per year.

Easy Ways to Save Money on Groceries and Food

Food is one of the most flexible categories in any budget — and one of the most common places people overspend without realizing it.

Cooking meals at home instead of ordering out is one of the fastest ways to cut expenses. The average restaurant meal costs three to five times more than making the same dish yourself. If your household spends $400 a month on takeout and restaurants, shifting half of that to home cooking could save $200 per month or more.

Here’s what actually helps:

- Meal plan before you shop. When you know what you need, you buy what you need. Less food waste, smaller grocery bills.

- Shop with a list. Going into a grocery store without a list is an invitation to spend money you didn’t plan to spend.

- Check the unit price, not the sticker price. The bigger box isn’t always cheaper per ounce.

- Eat what you buy. Food waste is one of the most invisible ways households lose money each month. Use what’s in your fridge before you buy more.

Save Money on a Tight Budget: The No-Spend Challenge

If you’re trying to save money fast and your margins are thin, the no-spend challenge is worth trying.

Pick a set period — one week, two weeks, a full month — and commit to spending only on true necessities: rent, utilities, groceries, transportation to work. No restaurants, no impulse buys, no online shopping. Just essentials.

It sounds harsh. Most people who try it say it’s easier than expected after the first two days. And it does two things at once: it pads your savings account quickly, and it helps you break the habit of spending money as a default activity. After the challenge ends, a lot of those spending habits don’t come back.

For anyone living paycheck to paycheck, a no-spend week can free up more cash in seven days than months of gradual cuts.

Building an Emergency Fund: The Foundation of Financial Stability

An emergency fund is not a luxury. It’s the thing that keeps one unexpected expense from wiping out everything you’ve worked to save.

Start an emergency fund before you tackle any other savings goals. Even $500 makes a real difference — it’s enough to cover a car repair, an urgent medical bill, or a missed paycheck without reaching for a credit card.

The standard target for emergency savings is three to six months of living expenses. If that sounds impossible right now, don’t let it discourage you. Start with $1,000. Then build from there.

Once you hit your target, don’t touch it for anything other than a genuine emergency. This isn’t your vacation fund, your new laptop fund, or your “I deserve a treat” fund. It’s your financial foundation. The peace of mind it provides is worth protecting.

Use Credit Card Rewards Without Carrying Debt

Credit cards get a bad reputation, but used correctly they’re one of the best tools for saving money on things you’d buy anyway.

Many credit cards offer 1–5% back on groceries, gas, travel, and dining. If you’re spending $500 a month on groceries and you put that on a card earning 3% back, that’s $15 back per month — $180 per year — just for swiping the right card on purchases you were making anyway.

The catch: you must pay your balance each month to avoid interest charges. The moment you carry a balance, the interest wipes out any rewards and then some. Use credit cards like a debit card — only spend what you have, pay it off in full, collect the rewards.

Mobile banking apps from most major banks make this easy to track in real time. Set up alerts for when your balance hits a certain amount, or enable auto-pay for the full balance each month so you never miss a payment.

Find Small Ways to Bring In Extra Income

Cutting expenses is only half the equation. The other half is adding to what comes in.

You don’t need a second job. There are practical ways to generate extra income without overhauling your schedule:

- Sell things you don’t use. Most homes have hundreds of dollars’ worth of items sitting in closets. A few hours on a resale platform can put real money in your pocket.

- Offer a skill locally. Dog walking, tutoring, lawn care, freelance writing, graphic design — skills people pay for are everywhere. Even a few hours a month at $25–$50/hour adds up.

- Rent what you own. A spare room, a parking spot, your car on weekends — peer platforms have made this easier than ever.

Put that money directly into your savings account before it mixes with your spending money. Even a few hundred extra dollars a month compresses your savings timeline significantly.

The Simplest Formula: Start, Automate, Review

Learning how to save money doesn’t require a finance degree. It requires three habits: start now (even with a small amount), automate your savings so you can’t spend it first, and review your budget monthly to catch what’s drifting.

Small changes today compound into significant savings over months and years. A $50/month automatic deposit at 4.5% interest grows to nearly $7,500 over ten years — and that’s before any increases. Start higher, add to it as your income grows, and the number gets much better.

You don’t have to save as much as someone else. You just have to start.