{kind=link}

Table of Contents

Pay day hits and the money’s gone by Thursday. You check your bank account on the 22nd and wonder where $400 went. Sound familiar?

About 65% of Americans have no idea how much they spend in a typical month. Not because they’re bad with money — because nobody ever sat them down and taught them how to make a budget that actually fits a real life.

A budget isn’t a punishment, and it’s not a spreadsheet of guilt. It’s a plan that tells your money where to go before it slips away. Done right, it takes about an hour to set up and 10 minutes a week to maintain.

Five steps below. None of them require math beyond fifth grade — but they’ll change how you spend your money.

What a Budget Actually Is (and What It Isn’t)

A budget is a plan for your money. That’s it. Money you have coming in, money going out, and what’s left over. It’s not about restriction. It’s about deciding in advance instead of regretting in arrears.

The budget isn’t there to make you feel bad. It’s there to help you reach your goals — whether that’s an emergency fund, paying off debt, saving for a vacation, or just not panicking on the 27th of every month.

A good budget shows you three things at a glance: how much money you have coming in, where it’s going, and how much you can put toward your money goals. Master those three and you’ve got control of your finances.

Some folks think budgeting means hours with a calculator and a spreadsheet. It doesn’t have to. Pen and paper, or a free budgeting app, can do the job in 30 minutes flat.

Step 1: Figure Out Your Monthly Income

Start with the money coming in. Your monthly income after taxes — your take-home pay — is the foundation of your budget. Not your gross salary, not what your offer letter said. The number that actually lands in your bank account.

If you have a salaried job with a steady paycheck, that part’s easy: multiply your bi-weekly take-home by 2.17 (which accounts for 26 paychecks a year), or just look at three months of bank statements and average them.

If your income changes month to month — freelance, commission, tips, side gigs — use the lowest three months of the last year as your baseline. Plan for the worst, save the surplus when you have a good month.

Don’t forget other sources of income: child support, rental income, side hustle earnings, regular dividend payments. Add them in.

This is the ceiling for everything that comes next. You can’t budget for money you don’t have.

Step 2: List Your Monthly Expenses

Now the harder part: figuring out where the money’s actually going. Pull up two or three months of bank and credit card statements and make a list of every recurring monthly expense.

Split everything into two columns.

Fixed Expenses

These are the bills that look about the same every month:

- Rent or mortgage

- Car payment

- Insurance (health, auto, renters)

- Subscriptions (streaming, gym, software)

- Loan payments

- Phone bill

A fixed expense doesn’t change much. You can negotiate some down or cancel subscriptions you don’t use, but otherwise these are your floor.

Variable Expenses

These shift month to month:

- Groceries

- Gas

- Eating out

- Utilities (which swing seasonally)

- Personal care

- Entertainment

Variable expenses are where most people overspend without noticing. Look at three months of data and the patterns jump out — the $200 in food delivery, the $80 in coffee, the random Amazon runs.

Don’t forget the once-or-twice-a-year stuff either: car registration, holiday gifts, vet visits, birthdays. Divide the annual cost by 12 and tuck a slice into your monthly budget every month so the big bills don’t blow it up.

Step 3: Set Your Financial Goals

A budget without goals is just bookkeeping. Decide what you’re working toward before you fight over the numbers.

Short-Term Goals (Under a Year)

- Build a starter emergency fund of $1,000–$2,000

- Pay off a credit card

- Save for a vacation

- Stop overdrafting

Long-Term Goals (One Year and Beyond)

- Build a full emergency fund of three to six months of expenses

- Pay off student loans

- Save a house down payment

- Start saving for retirement

- Invest your money for the future

Write these down. Specifically. “Save more” is not a goal. “Put $300 a month into a Roth IRA” is a goal. The specificity is what lets you carve room in your budget to actually fund them.

Most people skip this step and wonder why their budget feels pointless. Goals are the reason you say no to the $7 latte. Without them, every purchase feels reasonable.

Step 4: Subtract Expenses from Your Income

Time for the math. Subtract your total expenses from your monthly income. Three things can happen.

Positive number. Money left over. Good — now you can direct that money toward your savings or debt. Pick a goal, name it, and move that amount automatically every payday.

Zero. Every dollar is spoken for, but nothing’s left for goals. You’ll need to cut back somewhere or earn more.

Negative number. You’re spending more than you bring in. This is the most common situation when people first create a budget — and it’s exactly why building a budget matters. You can’t fix what you can’t see.

If you came out negative, look at your variable expenses first. Where are you spending the most money? That’s where the easy cuts live. Eating out, subscriptions you forgot about, the $40 a month in delivery fees you didn’t realize added up.

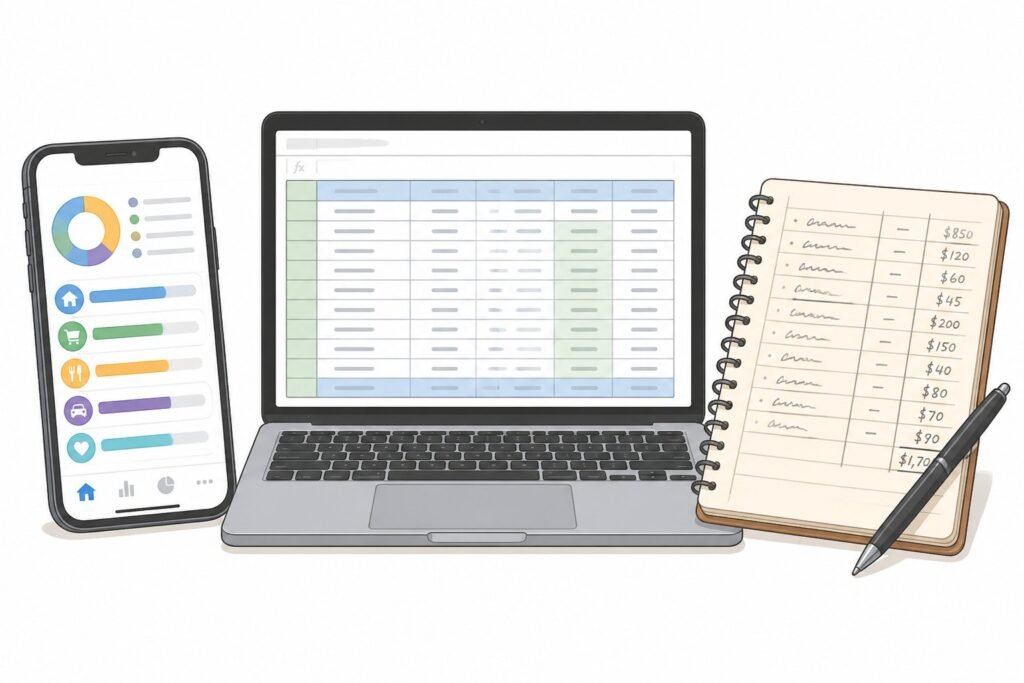

Step 5: Pick a Budgeting Tool That Fits You

The best way to budget is the one you’ll actually use every month. Here are the four main options.

Pen and Paper

Old school but it works. A notebook, your numbers, updated weekly. Slow but it forces awareness. If you’re the kind of person who needs to write things down to remember them, start here.

A Spreadsheet

Free, flexible, lives forever. Google Sheets or Excel. Plenty of free budget templates exist online — search “Google Sheets budget template” and you’ll find a dozen ready to copy. Best if you like seeing all your numbers in one place.

A Budgeting App

Apps like YNAB, Monarch, EveryDollar, or Copilot connect to your accounts and auto-categorize transactions. Some are free, some are $10–15 a month. Worth it if you’ve tried tracking manually and keep falling off. The automation does the heavy lifting.

A Budget Calculator

For first-timers, even a basic online budget calculator (NerdWallet and Bankrate both have free ones) can help you find rough percentages — like the 50/30/20 rule that says spend 50% on needs, 30% on wants, 20% on savings or debt.

Don’t agonize over the tool. The simplest one you’ll open every week beats the perfect one you’ll abandon in February.

How to Actually Stick to Your Budget

Building a budget is the easy part. Sticking to it is where most people fall off.

A few things that genuinely help:

- Automate the savings first. The day your paycheck hits, move money to your savings account before you have a chance to spend it. Pay yourself first. Always.

- Use cash or a separate debit card for variable categories. Withdraw your weekly grocery and entertainment budget in cash, or use a checking account with just that amount. When it’s gone, it’s gone.

- Check in weekly, not daily. Daily tracking burns people out. Once a week, 10 minutes, see where you stand.

- Give yourself a “fun money” line. A realistic budget includes things you want — not just bills. Cut all the fun and you’ll quit in three weeks.

- Forgive a bad week. Overspent on Saturday night? Adjust your spending for the next two weeks instead of throwing the whole thing out.

The people who stick to a budget aren’t more disciplined than you. They’ve just set things up so they don’t have to be.

Common Budget Mistakes That Wreck It

A few traps people fall into when they first try to make a budget:

Setting it too tight. If your budget for groceries is $200 and you spend $400, the budget’s wrong, not you. Start with what you actually spend, then trim.

Forgetting irregular expenses. Car repairs, gifts, annual subscriptions. They’ll come. Build a small monthly buffer for them.

Tracking but never reviewing. Watching numbers tick by without acting on them is busywork. Each month, ask: did this work?

Comparing your budget to someone else’s. Your budget has to fit your life, not Reddit’s. Someone in Mississippi paying $900 rent and someone in NYC paying $3,200 aren’t in the same conversation.

Quitting after one bad month. Everyone has them. The point isn’t perfection. It’s the trend over six months.

Review Your Budget Every Month

A budget isn’t a one-time setup. Life changes, prices change, goals shift. Review your budget at the end of every month and make adjustments.

Ten minutes is enough. Open last month’s numbers and ask:

- Where did I overspend?

- Where did I have extra money?

- Did any new expenses pop up?

- Did I hit my savings goal?

- Do I need to create a new budget category, or kill one?

If a line keeps going over by 20% three months running, that line is wrong — fix it instead of fighting it. If you keep coming in under in another category, move that money toward savings or debt.

This monthly check is the single thing that separates people who actually win at managing their money from the people who quit by March.

Your First Move

If you’ve read this far, the only thing left is to actually open something — a notebook, a spreadsheet, an app — and write down your monthly income. Just that one number.

Once that’s down, the rest is filling in blanks. Most people who give it 60 minutes on a Sunday afternoon have a working budget by dinner.

Your money is already moving somewhere every month. Budgeting just means you decide where, instead of finding out after.